When Lower Prices Don’t Mean Lower Costs: How Part D Benefit Changes Are Shifting Out-of-Pocket Spending in 2026 Under the Inflation Reduction Act

Plan design changes following the IRA may be increasing beneficiary cost exposure even as drug prices decline.

Background

In 2026, the Inflation Reduction Act (IRA) changed the Medicare Part D benefit in several important ways, including a redesigned benefit with a maximum out-of-pocket cap (MOOP) of $2,100 and the implementation of Maximum Fair Prices (MFPs) for initial price applicability year (IPAY) 2026 selected drugs. The redesigned benefit resulted in changes to Part D plan financial responsibilities, including increased plan responsibility in the catastrophic phase of the benefit.

In response to increased financial responsibility, research suggests that plans have shifted their benefit designs toward coinsurance in the initial coverage phase and/or higher deductiblesi. Because of this shift, beneficiaries may be paying more out of pocket for some IPAY 2026 selected drugs than they did before the IRA.

To understand what has changed, our analysis used Part D formulary data files to examine shifts in plan coverage of selected drugs between 2023 (before the IRA was implemented) and 2026.

What We Found

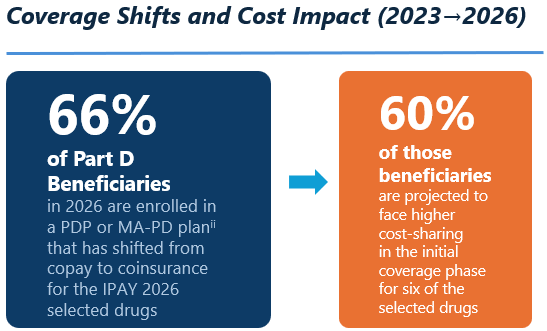

- Copay to coinsurance shifts is widespread and often increases cost-sharing even with MFPs

In 2026, about two-thirds (66%) of Part D beneficiaries are enrolled in a standalone prescription drug plan (PDP) or Medicare Advantage Prescription Drug (MA-PD) planii that has shifted coverage of IPAY 2026 selected drugs from a fixed copay to coinsurance between 2023 and 2026. Among these beneficiaries, about 60% are projected to face higher cost-sharing after reaching the deductible and before the maximum out-of-pocket cap (ie, the initial coverage phase) than they would have faced in 2023. For the millions of beneficiaries who take one of six IPAY 2026 selected drugs, out-of-pocket increases could range from 22% to 118%iii. - Specialty-tier drugs can show “savings,” but the impact may be limited

For specialty-tier drugs, beneficiaries may experience savings because these drugs were previously largely subject to coinsurance. However, many beneficiaries using these therapies reach MOOP, so the impact of MFP may be limited, suggesting that the MOOP may be more effective at limiting beneficiary out-of-pocket cost exposure than MFPs.

- Premium and deductible increases add additional exposure

These same Part D plans have also increased premiums and deductibles from 2023 to 2026, further exposing beneficiaries enrolled in these plans who use any of these six IPAY 2026 selected drugs to higher out-of-pocket costs. Among beneficiaries who see an increase, the combined premium-and-deductible impact averages $338 more per year.

Why It Matters

Overall, these findings suggest that MFPs do not guarantee savings for Part D beneficiaries and may increase costs for many. They also reinforce that Part D plan benefit design, including utilization management like step therapy and prior authorization, continues to play a significant role in shaping beneficiary access to medicines, including selected drugs and their therapeutic alternativesiv. More broadly, CMS’s price-setting program appears to do little to protect many beneficiaries from potentially harmful Part D plan actions and may even increase the risk of therapy delays and access limitations.

i https://schaeffer.usc.edu/research/cost-sharing-burden-medicare-part-d

ii Excludes Special Needs Plans (SNPs), Medicare-Medicaid Plans (MMPs), Employer Group Waiver Plans (EGWPs), Programs of All-Inclusive Care for the Elderly (PACE) plans, and Part B-only plans.

iii Fiasp/Novolog is not included in the analysis due to the IRA provision that caps monthly cost-sharing at $35.

iv https://www.iqvia.com/locations/united-states/library/white-papers/the-impact-of-formulary-controls-on-medicare-patients-in-five-chronic-therapeutic-areas